If you’ve come across the term cyclemoneyco, you’ve probably wondered whether it refers to a company, a financial system, or just another trending keyword floating through digital finance communities. The truth is more nuanced. In 2025, “cyclemoneyco” functions less like the name of a single regulated institution and more like a label attached to ideas about automated money flow, algorithmic trading, and smarter cash-management systems. It’s used heavily in blog posts, fintech commentary, and social media discussions that promise faster financial growth and continuous cash efficiency.

This article explains what cyclemoneyco usually refers to, how the underlying idea of money cycling works, the risks people need to understand, and how to safely implement the beneficial parts of the strategy in your own life. Instead of hype or vague claims, you’ll find a grounded explanation based on practical financial behavior and the current realities of digital money management.

The Rise of the CycleMoneyCo Concept

In modern personal finance, the central challenge is balancing liquidity, growth, and risk. Rising inflation, volatile markets, and the increasing number of people managing irregular income streams have all pushed consumers toward automation. That’s part of why cyclemoneyco content has taken off. The term is often positioned as a smart way to “keep your money cycling” instead of allowing value to erode in low-yield accounts.

The dramatic visibility of this term stems from three trends. First, people are tired of slowly losing purchasing power when savings sit untouched. Second, the fintech ecosystem has pushed automation deeper into daily money decisions, from automatic bill-pay to real-time investment algorithms. Third, many creators and commentators have framed cyclemoneyco as a modern shortcut for wealth building, even though the underlying principles are as old as budgeting itself.

Because its usage varies widely across platforms, the safest approach is to treat cyclemoneyco as a concept rather than as a predetermined product. That mindset lets you focus on the core ideas without falling for exaggerated promises.

What CycleMoneyCo Most Often Refers To

Despite the inconsistent definitions across different sources, cyclemoneyco content tends to fall into three recurring interpretations.

One interpretation treats CycleMoneyCo as an automated micro-investing or algorithmic trading tool. In these explanations, users deposit funds into a dashboard that executes many small trades throughout the day, usually in digital assets, forex pairs, or other volatile markets. The goal is to capture small, repeated price movements. Sometimes users are offered risk settings, stop-loss rules, and toggles for reinvesting profits.

Another interpretation presents CycleMoneyCo as a cash-flow optimizer. Here, the system sits on top of your existing financial accounts and moves cash automatically between spending accounts, savings, and investment vehicles. When income arrives, the algorithm allocates it toward bills, reserves, and potential growth opportunities. It adjusts the amounts in real-time as spending patterns change.

A broader interpretation describes cyclemoneyco as a philosophy: a structured money life where cash moves in a cycle of earning, allocating, investing, and reinvesting. This lens is less about a specific tool and more about adopting a continuous financial loop that maximizes the productivity of each dollar.

These interpretations share a common thread: they frame money as something in motion, not something that rests.

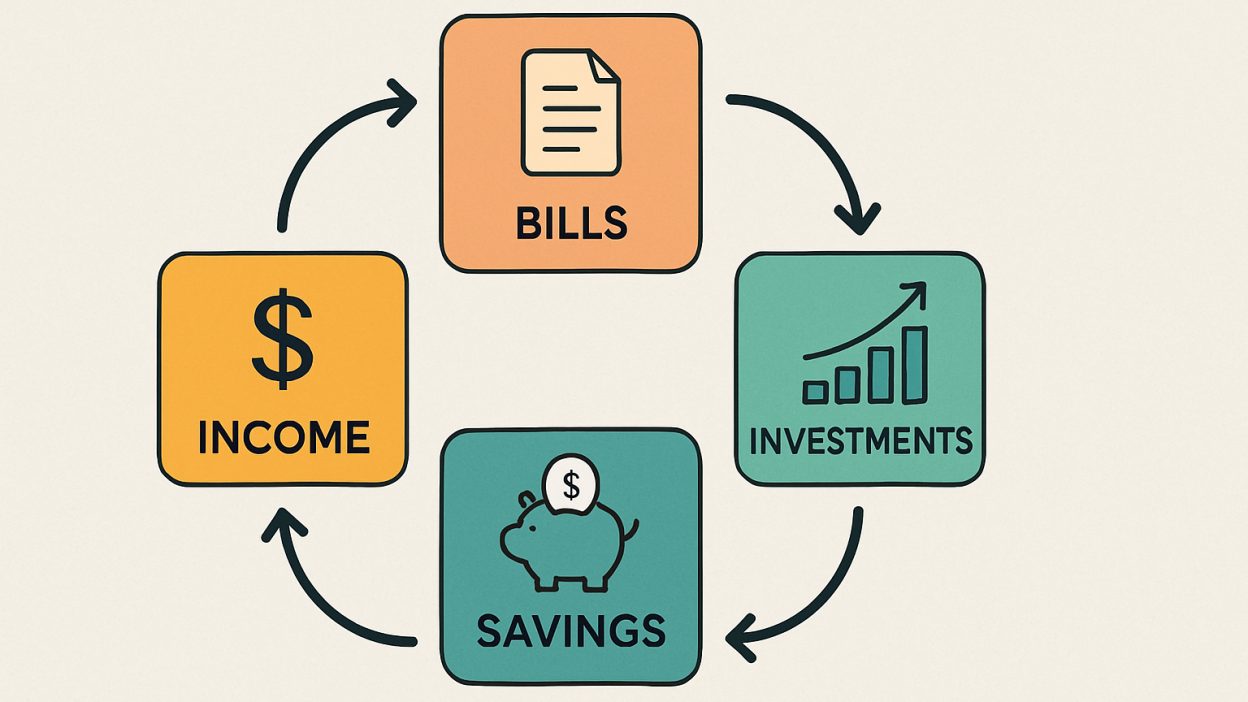

The Core Idea Behind Money Cycling

Whether you call it cyclemoneyco or simply smart money management, the root principle remains that money should move through a deliberate loop instead of stagnating. The loop usually starts with income, flows into fixed expenses, continues into reserves for emergencies, and ultimately reaches long-term investments. When those investments produce returns, the returns are fed back into the system rather than withdrawn prematurely.

This model offers clarity. Many households struggle because their money moves haphazardly. Income arrives and disappears without passing through intentional stages. A cycle-based structure forces you to define what happens to each dollar at each step. Over time, that structure builds momentum.

Continuous reinvestment, even on a small scale, is the defining feature of compounding. Most people understand compounding intellectually, yet few adopt the habits required to let it work. A cyclemoneyco approach emphasizes that compounding is not an event but a process sustained by repeated movement.

How CycleMoneyCo Platforms Claim to Operate

Although the name isn’t tied to a single verified institution, many descriptions of CycleMoneyCo-style platforms follow similar patterns, especially in how they describe automation and user experience.

The first pattern is algorithmic execution. In these models, the system uses pre-defined rules or machine-learning signals to open and close trades. Users often see dashboards filled with small positions, rapid turnover, and real-time gains and losses. These systems promise to remove emotion from investing and rely on speed, consistency, and micro-opportunities. While this can theoretically work in certain market structures, it also carries high volatility and no guarantee of profit.

Another pattern is cash-flow balancing. This model analyzes deposits, bills, subscription charges, spending behavior, and cash needs. It attempts to keep just enough in checking to avoid overdrafts while moving surplus cash toward higher-yield locations. This type of automation appeals to individuals who struggle with manual money organization or who maintain multiple accounts with inconsistent balances.

The third pattern is incentive-driven engagement. Some platforms combine dashboards with gamified features, weekly scorecards, or referral rewards. While gamification can improve engagement, it must be approached carefully. Financial decisions should reflect goals, not the pursuit of badges or bonuses.

Understanding these mechanics is important because marketing language often glosses over limitations. Automation can be useful, but it cannot remove risk. Every system must be evaluated on its transparency, track record, and regulatory status—not just its interface.

Potential Advantages of a CycleMoneyCo Approach

If you focus on the underlying concept rather than the branding, several potential benefits emerge. One advantage is clarity. When your finances follow a predictable loop, your money has structure, and decisions become easier. Instead of guessing where your paycheck will go, you rely on a system.

Another advantage is improved resilience. People who cycle money intentionally tend to build emergency buffers naturally because the system prioritizes them. In financially unstable environments, that buffer is essential.

The approach also helps combat the silent loss of value caused by inflation. When excess cash moves regularly into growth-oriented accounts, its long-term purchasing power has a better chance of being preserved. In the past few years, as inflation has fluctuated, households with structured allocation habits have generally fared better than those with scattered banking behavior.

Automation can also reduce emotional decision-making. For many, the hardest part of saving or investing is not understanding the mechanics but maintaining discipline. If transfers occur automatically on payday, the decision is made before temptation appears.

These benefits are real, but they require thoughtful implementation. Blind automation can be as harmful as no automation at all.

Risks and Concerns Surrounding CycleMoneyCo

Because the term “CycleMoneyCo” is used so broadly, it’s crucial to approach any platform or service using that label with careful scrutiny. The first major concern is opacity. Without clear regulatory documentation, audited financial reports, or verifiable leadership, a platform’s credibility becomes difficult to assess. Financial tools work best when the underlying mechanics are transparent.

Market risk is the second issue. Algorithmic trading systems, especially those operating in volatile markets, can produce rapid gains during stable periods and sudden losses during unpredictable swings. People often forget that automation does not eliminate downside volatility. In fact, automated strategies can accelerate losses when markets move faster than their rules anticipate.

Platform risk is another concern. Even a legitimate tool depends on its infrastructure. Bugs, downtime, security weaknesses, or poor data handling can expose users to losses unrelated to market performance. When a system connects directly with bank accounts or exchanges, safety demands extremely robust practices.

Finally, there is psychological risk. The promise of continuous cycling and constant profit can lure people into believing that growth will always compound without interruption. No system can offer that. Healthy financial habits require a realistic understanding of uncertainty.

The cyclemoneyco idea is not inherently dangerous, but trusting opaque versions of it can be.

How to Safely Implement a CycleMoneyCo Strategy Yourself

You don’t need any CycleMoneyCo-branded platform to benefit from the positive parts of money cycling. You can create your own structured cash-flow system using standard, regulated accounts.

Start by mapping your personal cycle. Identify where your income enters, where fixed expenses exit, and what percentage should move into savings each month. A simple framework might allocate a predictable portion to bills, a portion to an emergency fund, and a portion to long-term investment accounts. The key is consistency. When each dollar has a predetermined destination, the cycle becomes self-sustaining.

Next, define the size of your emergency buffer. This amount should reflect your monthly essentials, job stability, and household obligations. Once the buffer reaches the desired level, your cycle can shift surplus cash toward higher-yield options rather than allowing it to overflow in checking.

Automation comes next. Setting up automatic transfers removes friction and strengthens discipline. Transfers scheduled for the same day income arrives can prevent accidental spending and reinforce the cycle. Investments can be automated through regulated brokers or retirement accounts.

The final step is regular review. A money cycle that once suited your life may need adjustment as income changes, family situations evolve, or new goals emerge. Quarterly reviews are often enough to ensure the system remains aligned with your needs.

This approach captures the essence of cyclemoneyco while avoiding unnecessary risk.

Who Benefits Most From a CycleMoneyCo Mindset

A money cycle is valuable for anyone seeking more structure, but certain groups may find it especially transformative. Freelancers and gig workers often experience irregular income. A cycle-based system helps stabilize cash flow, ensuring that bills, taxes, and reserves are covered before lifestyle spending expands.

Small business owners also benefit. When business revenue flows unpredictably, a structured cycle helps manage working capital, maintain operational reserves, and reinvest profit strategically. A disciplined cycle can prevent businesses from overspending when revenue spikes or under-investing when growth opportunities appear.

Individuals with inconsistent savings habits often benefit as well. A cycle reduces reliance on willpower and turns financial progress into a routine. Over time, that routine builds confidence.

At the same time, some people should avoid aggressive implementations of money cycling. Anyone with high-interest debt, dangerously low savings, or high anxiety around investing should focus on fundamentals first. Money cycling works best when built on a stable foundation.

Common Questions About CycleMoneyCo

Many readers ask whether CycleMoneyCo is a real company. Today, it functions more as a digital finance term than as a single regulated brand. Various websites describe tools or services using the name, but they do not represent a unified institution with a clear public record.

Another common question is whether cyclemoneyco is a scam. The concept itself is not. The idea of moving money intentionally is standard in personal finance. The risk comes from platforms that borrow the name without offering transparency. As with any online financial tool, users should verify regulatory status, avoid guaranteed-profit claims, and stay cautious if pressured to invest quickly.

A final question is whether money cycling can really increase wealth. When applied responsibly, structured cash flow and consistent investing can improve long-term outcomes. However, no algorithm or automation can guarantee returns. Growth comes from disciplined behavior, not from brand names.

Also Read: Problem on Llekomiss Software: Causes & Fixes

Final Thoughts: Treat CycleMoneyCo as a Framework, Not a Shortcut

The term cyclemoneyco may continue appearing in digital finance content, but you don’t need a specific app or platform to apply its best ideas. The true value of the concept lies in adopting a clear cycle that guides your money consistently through earning, saving, investing, and reinvesting.

When executed with transparency and discipline, this approach can bring more stability, more intentionality, and stronger long-term financial health. When executed blindly, especially through opaque systems, it can expose people to unnecessary risk.

Think of cyclemoneyco not as a magic tool, but as a reminder that money grows when it moves with purpose. If you build your own cycle around that principle, you capture the benefits without depending on a system you can’t verify.